Clients who reduce or eliminate their allocations to risk assets ahead of a catalyst event such as the 2020 US elections, or clients who find themselves in sudden possession of a large chunk of cash either by inheritance, earnings or windfall face a daunting challenge. While allocating at least some portion of investor portfolios to equities is the best way to grow and preserve real purchasing power, equities can be volatile and the prospect of investing a lump sum only to see it diminish by 10%, 20% or more in a short time is daunting. What is the best course of action?

Historically, the best returns have come by taking the plunge, living with the risk and investing the full lump sum at once in whatever equity allocation is deemed best based on the client’s age, income, goals, risk tolerance and other considerations.

- While this lump sum approach has poor short-term returns should the investor be unlucky enough to invest immediately before a sharp drop, the baseline frequency of corrections, recessions or depressions is low and the odds are in the investor’s favor.

- In any given month, it’s statistically more likely that the market will rise than fall, and therefore lump sum investing is theoretically the best course of action.

-

-

- Using the S&P500 index in the period from 1/2/90 to 11/25/20 (the last date with 256 subsequent trading days), 66% of all 30 trading-day periods showed positive returns on a total return basis.

-

- Other avenues are available for those fearful of poor timing luck or less sanguine about the market’s short-term return prospects. The classic method to put cash to work is dollar-cost-averaging, investing in tranches at preset time horizons. Value averaging, where the investor sets a predetermined return goal then invests slower or faster depending on whether the market is rising or falling (presumably offering worse/better value per dollar invested) is another alternative.

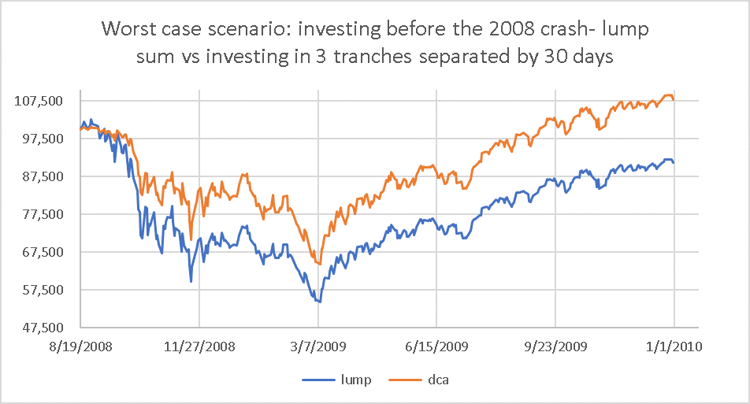

Here is a graph showing the result of investing at the worst time within this sample period, shortly before the Great Financial Crisis:

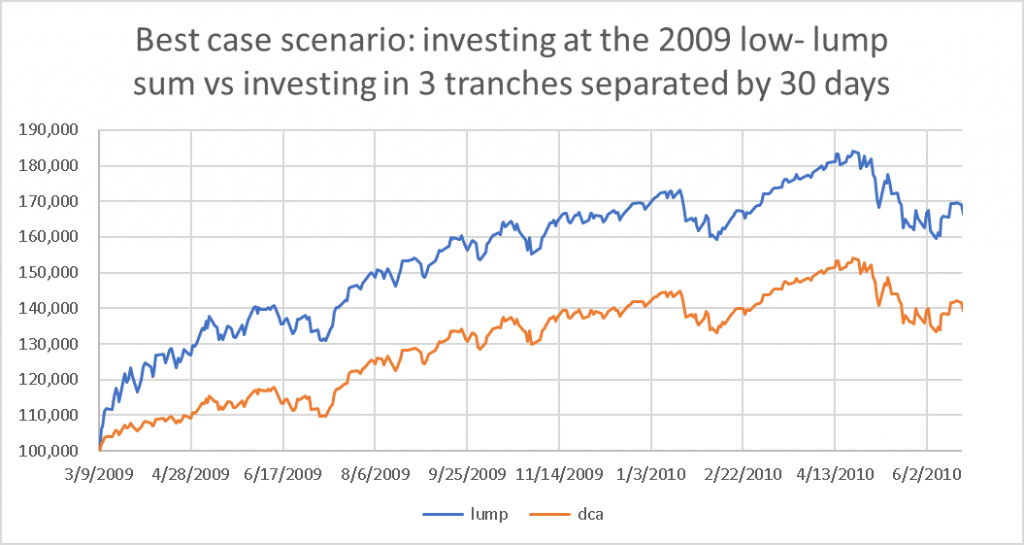

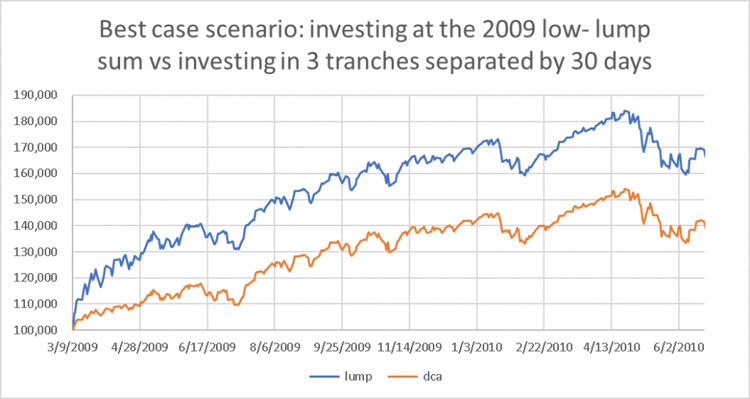

Here is a graph showing the result of investing at the best time within this sample period, at the Great Financial Crisis lows:

- A realistic assessment of risk tolerance on the part of the advisor and the client is critical in determining asset allocation; if a correction leads the client to consider reducing their equity allocation then the starting allocation may have been too high for their risk tolerance.

-

- It’s tempting to add more equities to increase long-term returns, especially given current yields on fixed income. However this approach could result in much lower returns if the excess allocation to equities is reduced at a market trough in response to losses.

- Some method of rebalancing to the target asset allocation either periodically or when preset guardrails are exceed has historically had a positive impact on returns and risk/reward.

- Frequent rebalancing between a risk-free asset with no return and a volatile asset with no return but high volatility can create a positive expected return on the portfolio, a neat magic trick!

- Exencial offers clients who are unusually risk-averse or simply bearish on a tactical basis several alternative routes to investing or reinvesting cash:

-

- EXE’s put-write strategy offers clients a predetermined route to invest in the event of a market decline, while earning income likely to exceed the returns on cash in the meantime.

- This approach risks buying too early in a decline or missing out on gains in a rally but offers a systematic plan and a yield greater than cash.

- This has the side-effect of making the decision to reinvest automatic should a selloff materialize, removing the temptation to wait for further market declines and potentially missing the opportunity.

- EXE’s put-write strategy offers clients a predetermined route to invest in the event of a market decline, while earning income likely to exceed the returns on cash in the meantime.

- For instance, should an investor in mid-August 2020 have been willing to buy 100 shares of SPY at a price of 320 or below, while the current spot price was $339.48, he or she could have sold Sep $320 puts and been paid $250 upfront for a return of 0.78% in 28 days. The put seller must be willing to purchase the stock at the strike price, even if the market price falls far below the strike, and thus acts as insurer to the put buyer and secures a return for this risk.

-

- EXE’s Defensive Equity and Hedged Equity portfolios offer conservative, lower-beta exposure to the long-term growth potential of equities.

- These strategies may be attractive as “on ramps” to investment in our Core, Select and Opportunity strategies.

- No investment comes without risk of loss, however depending on the approach, the maximum loss may be reduced as compared to a traditional equity allocation.

- EXE’s Defensive Equity and Hedged Equity portfolios offer conservative, lower-beta exposure to the long-term growth potential of equities.

Jon Burckett-St. Laurent

Senior Portfolio Manager