Paying taxes on income, dividends and investment gains is likely a sign that assets are being productive and are generating cash flows and appreciation, which is ultimately the goal for investors. That said, taxes are still a cost of investing. They can drag net investment returns lower and, as assets grow over time, begin to create complexities and reduced planning flexibility. For this reason, current and future taxes should ideally be managed and investments aligned with planning goals in a cohesive strategy.

One way to do so is by utilizing asset location1, the thoughtful positioning of an investment into a complementary account type. For instance, many investors hold both stocks and bonds, which are taxed differently. Several investors also have both joint and individual taxable accounts, as well as IRA and 401(k) accounts, which are all taxed differently. The decision to place stocks in one account (let’s say a joint account) and bonds in another account (the IRA) would be considered an asset location decision.

Done properly, asset location can provide immediate and future tax and planning benefits. While the benefits will depend on individual circumstances, several studies have estimated how much asset location can improve annual net returns. A Vanguard study estimated asset location can add up to 0.75 percent annually to returns.2 When coupled with a withdrawal strategy, Morningstar found that asset location can provide an estimated 0.23 percent annual benefit on net returns.3

Asset location is a behavioral item that could add value to investor returns.

Investor Returns = Market Returns – Costs ± Investor Behavior

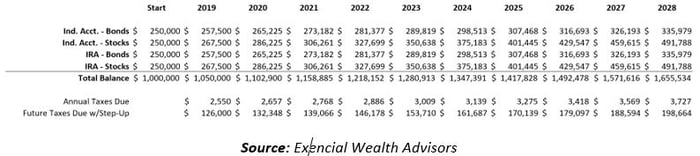

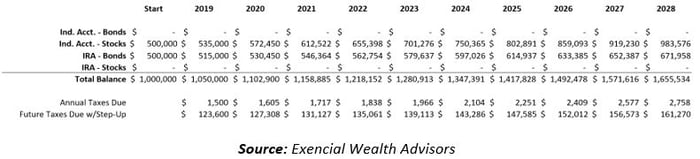

Let’s assume an investor has $500,000 in an individual taxable account and $500,000 in an IRA without plans to spend these dollars. This investor wants to hold 50 percent in stocks and 50 percent in bonds. If the investor does not utilize asset location, both accounts will be invested in the same way. Below are the results assuming heirs inherit the assets in 10 years.

However, if the investor locates all the stocks in the individual taxable account and all the bonds in the IRA, the estimated asset location benefit is 0.28 percent per year. In this example, the investor will save about $1,000 per year in taxes and about $37,000 in future taxes due on the IRA assets.

Assumptions: No spending or rebalancing of assets. Bonds pay 3 percent in taxable interest with 3 percent total return. Stocks pay 2 percent in qualified dividends with 7 percent total return. Capital gains rate is 15 percent. Income tax rate is 24 percent. At death, heirs receive a step up and cash out IRA entirely. Taxes are paid with cash held outside these accounts.

With the goal of improving planning outcomes and after-tax returns for clients, Exencial considers several factors before executing an asset location strategy, including:

- Tax rates: We need to know the client’s effective federal income tax rate, capital gains rate and state income tax rate as well as projected future tax rates.

- Spending needs: Cash flow analysis and income needs will influence how assets are distributed across account types.

- Beneficiaries: The asset location recommendation will be affected by who will eventually receive the remaining assets.

- Individual/joint/trust accounts: The appreciation of assets held in these accounts can be taxed at favorable capital gains rates, and assets will generally receive a step-up in basis at death.

- IRAs/401(k) plans: IRAs and 401(k) plans represent present tax savings but future income tax liabilities. Because these accounts may have lower expected returns than other accounts, they are typically good assets to leave to charity.

- Roth IRAs: If the client owns a Roth IRA, they should consider designating family members as beneficiaries and hold the highest expected returning assets here. An investor could also consider converting assets into a Roth IRA.

- Rebalancing: If rebalancing is expected, we will need to plan on holding enough assets in IRAs and Roth IRAs to facilitate this.

To realize the current and future benefits of asset location, the investment, planning and tax considerations need to be integrated within an investor’s strategy. Exencial thoroughly evaluates a client’s situation before executing asset location, and the strategy may need to be updated over time, especially as tax laws evolve. If you have questions about asset location or would like additional information, please contact your Exencial advisor.

Sources:

1. Investopedia – Minimize taxes with asset location

2. Vanguard – Putting a value on your value: Quantifying Vanguard Advisor’s Alpha®

3. Morningstar – Alpha, beta, and now…Gamma

PAST PERFORMANCE IS NOT AN INDICATION OF FUTURE RETURNS. Information and opinions provided herein reflect the views of the author as of the publication date of this article. Such views and opinions are subject to change at any point and without notice. Some of the information provided herein was obtained from third-party sources believed to be reliable but such information is not guaranteed to be accurate. In addition, the links provided within are for convenience only and the provision of the links does not imply any sponsorship, endorsement, or approval of any of the content. We do not guarantee the content or its accuracy and completeness. The content is being provided for informational purposes only, and nothing within is, or is intended to constitute, investment, tax, or legal advice or a recommendation to buy or sell any types of securities or investments. The author has not taken into account the investment objectives, financial situation, or particular needs of any individual investor. Any forward-looking statements or forecasts are based on assumptions only, and actual results are expected to vary from any such statements or forecasts. No reliance should be placed on any such statements or forecasts when making any investment decision. Any assumptions and projections displayed are estimates, hypothetical in nature, and meant to serve solely as a guideline. No investment decision should be made based solely on any information provided herein and the author is not responsible for the consequences of any decisions or actions taken as a result of information provided in this book. There is a risk of loss from an investment in securities, including the risk of total loss of principal, which an investor will need to be prepared to bear. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be profitable or suitable for a particular investor’s financial situation or risk tolerance. Exencial Wealth Advisors, LLC (“EWA”) is an investment adviser registered with the Securities & Exchange Commission (SEC). However, such registration does not imply a certain level of skill or training and no inference to the contrary should be made. EWA may only transact business in those states in which it is registered, notice filed, or qualifies for an exemption or exclusion from registration or notice filing requirements. Complete information about our services and fees is contained in our Form ADV Part 2A (Disclosure Brochure), a copy of which can be obtained at www.adviserinfo.sec.gov or by calling us at 888-478-1971

![]()